Justin Calheno

LUDLOW

VICE PRESIDENT, BUSINESS DEVELOPMENT OFFICER, RETAIL LENDING

NMLS #5549

jcalheno@countrybank.com

Direct Dial: 413-277-2370

Cell: 413-626-0395

You do many hard things in life, buying your home shouldn’t be one of them. Our mortgage experts will guide you every step of the way so you are well-prepared and set up for financial success.

Flexibility makes a difference! Select an adjustable-rate construction loan or a fixed-rate construction loan depending on your ideal rate and repayment schedule.

Building your dream home has never been more affordable! Take advantage of our competitive construction loan rates and finance up to 90%1 of everything from the foundation to the finishing touches! Even better, only pay interest during the first 12 months!

Construction loans cover up to 90%1 of the total cost of building a home as well as the cost of land, labor, materials, and permits. Once you are approved, you can access the money you need alongside each phase of the construction directly through your Country Bank checking account.

When the home or major renovations are complete, your construction loan will be converted into a traditional mortgage and you’ll begin making payments on the principal and interest. Sound like the right option for your needs? Apply now using our easy application or contact our experienced mortgage experts today with any questions.

Not finding your ideal home in Massachusetts? No problem! Bring your vision to life with a construction loan through Country Bank. Applying for a construction loan is easy! Check out what you can expect throughout the process:

Finalize your application with Country Bank and manage your money easily with our state-of-the-art Construct portal. Inside this portal you can monitor your project progress in real time, order inspections as needed, check your loan balance, collaborate with your builder, and get things done faster! If you are unsure if a construction loan is right for your project, please get in touch with one of our experienced mortgage experts today.

When you’re applying for a mortgage, it’s important to have someone you trust at your side. We’re experts at walking you through the entire process, answering your questions, and cheering you on to success. It’s what we’re made to do.

LUDLOW

VICE PRESIDENT, BUSINESS DEVELOPMENT OFFICER, RETAIL LENDING

NMLS #5549

jcalheno@countrybank.com

Direct Dial: 413-277-2370

Cell: 413-626-0395

SPRINGFIELD & SURROUNDING AREAS

AVP, MORTGAGE & COMMUNITY DEVELOPMENT OFFICER

NMLS #689658

lsanchez@countrybank.com

Direct Dial: 413-277-2041

Cell: 413-209-4823

Bilingual

Servicio en Español

CHARLTON, PAXTON, WEST BROOKFIELD & SURROUNDING AREAS

RETAIL LOAN OFFICER

NMLS #1687192

sdesantis@countrybank.com

Direct Dial: 413-277-2114

Cell: 413-302-3467

HOLDEN, SHREWSBURY, WESTBOROUGH & SURROUNDING AREAS

RETAIL LOAN OFFICER

NMLS #1650773

dgentleman@countrybank.com

Direct Dial: 413-277-2058

Cell: 774-502-7578

LEICESTER, WORCESTER & SURROUNDING AREAS

RETAIL LOAN OFFICER

NMLS #432698

kkemp@countrybank.com

Direct Dial: 413-277-2383

Cell: 774-200-5017

BELCHERTOWN, LONGMEADOW & SURROUNDING AREAS

RETAIL LOAN OFFICER

NMLS #432695

jsoucia@countrybank.com

Direct Dial: 413-277-2348

Cell: 413-262-2141

BRIMFIELD, PALMER, WARE & SURROUNDING AREAS

RETAIL LOAN OFFICER

NMLS #618959

jvelez@countrybank.com

Direct Dial: 413-277-2318

Cell: 413-636-2925

This calculator is for informational purposes only and its use does not guarantee an extension of credit. Your actual term and payment will be provided upon acceptance of a Country Bank Loan.

Take control of your future finances and set yourself up for success by making informed mortgage choices today.

We have you covered! Here is the information you’ll need when you are ready to apply for a mortgage.

STEP 1: GET PRE-QUALIFIED TO MAKE YOUR PURCHASE

Fill out a mortgage application for a prequalification. As part of this process we will obtain your credit report and request income documentation. We will then determine the amount you would be approved for and issue a prequalification letter. This letter can be used to put in an offer on a home.

STEP 2: APPLYING FOR YOUR MORTGAGE LOAN

If you are purchasing a property, you will want to contact your loan officer to get your mortgage application started and submitted once an offer is accepted. If you already own the property than simply reach out to a loan officer to get the mortgage application started and submitted.

STEP 3: REVIEW LOAN ESTIMATE

Once we have received and processed your submitted mortgage application, you will receive your initial loan disclosure paperwork which includes your loan estimate which includes a breakdown of potential closing costs and an estimated sum of necessary funds needed to complete your transaction.

STEP 4: PROPERTY APPRAISAL

Once you have reviewed your initial disclosure package and signed your intent to proceed. The appraisal fee will be collected and your appraisal will be ordered. The property will be appraised to establish its current market value.

STEP 5: UNDERWRITING PROCESS

The Loan Processor will submit your paperwork to a Residential Mortgage Underwriter who will underwrite this file to secondary market guidelines.

STEP 6: LOAN APPROVAL PACKAGE

After underwriting has approved your mortgage, the loan approval package will be sent out to you. Typically, this package will contain any outstanding loan conditions that are needed before the closing can be scheduled with the attorney. Once underwriting has received and reviewed the outstanding conditions, the loan will be cleared to close. At that point you will begin to work on scheduling the closing with your attorney. At least three days before your closing, you will receive your initial closing disclosure. This is a very important document as it breaks down the amount needed to bring to the closing.

STEP 7: CLOSING

The “closing” is the last step in buying and financing a home. This is when you and all the other parties in a mortgage loan transaction sign the necessary documents. Before you sign, make sure you carefully read and understand all the loan documents.

Credit requirements are dependent on many different factors, including the loan program applied for. If you are unsure of how your credit history will affect your application, please contact one of our loan officers who will discuss options with you.

Closing costs are the fees you pay to complete your loan; they include but are not limited to origination fee, title insurance, prepaid escrows, and more. Closing costs will vary depending on many different factors including the loan program applied for, down payment, etc. Your loan officer will provide you with a loan estimate that will break down expected closing costs.

DISCLOSURES:

Private Mortgage Insurance (PMI) required if the down payment is less than 20%.

1 If using a Licensed General Contractor, Country Bank will finance up to 90% of the appraised value of the property. If operating as your own General Contractor, Country Bank will finance up to 80% of the final value of the property.

Experience the difference of exceptional service when you stop by a local banking center.

Connect with your local banker by calling 800-322-8233 or sending an email to info@countrybank.com.

Manage your accounts from the palm of your hand whenever it’s convenient for you.

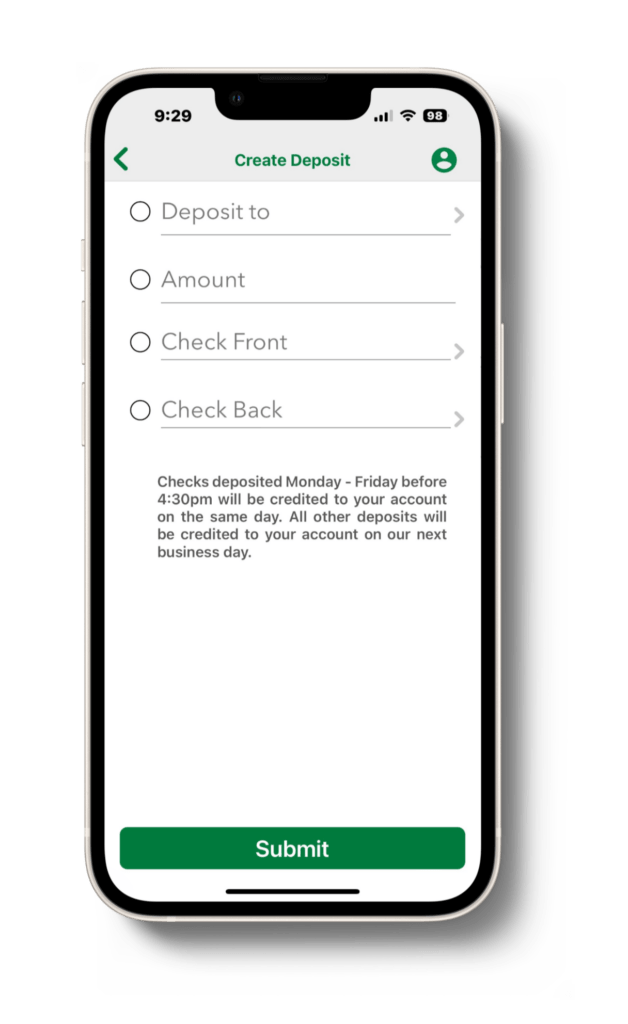

Deposit checks with the snap of a photo.

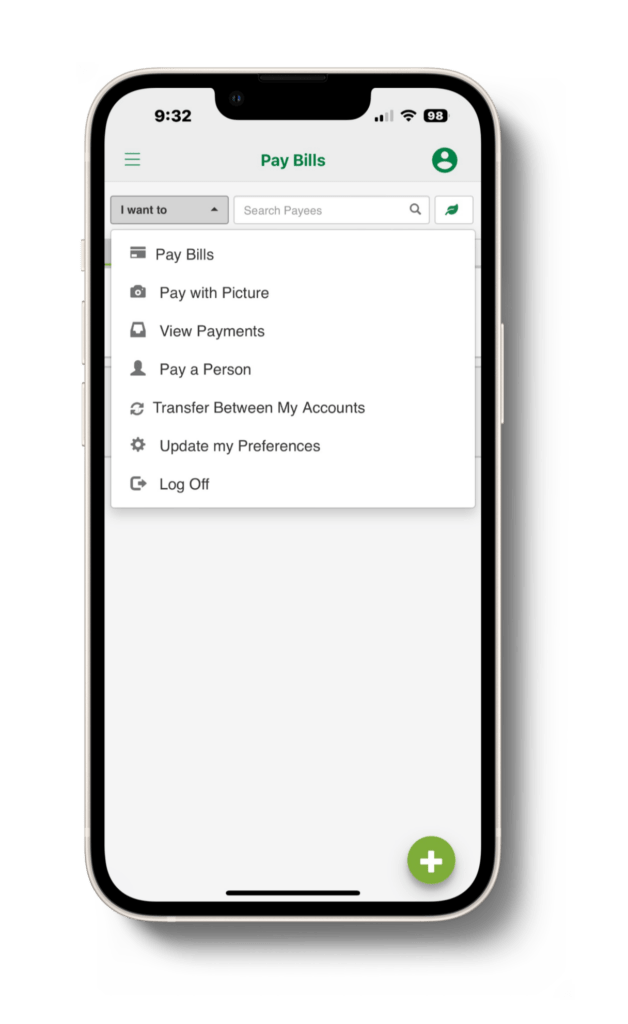

Easily transfer money between your accounts or over to a friend or family member straight from the Mobile App.